There is a strange meme going around since the health insurance exchanges opened up on October 1st — albeit it has been around before then. Apparently under the Affordable Care Act (ACA), people are provided various products and services for “free.” The one example being trumpeted most loudly is this bizarre notion that women are getting “free” birth control because of Obamacare. This access to “free” healthcare products and services has been celebrated by the left and maligned by the right.

Yet in order to believe that Obamacare provides “free birth control” requires complete ignorance of how insurance works.

It’s pretty easy to utilize this tagline as a cause for celebration or angry hand-wringing when the majority of the population doesn’t know the technicalities of what “insurance” means. Inevitably, what inspired me to write this was an e-mail sent out by the Democratic party on Sunday, October 6th:

Allow me to take this opportunity to cut through the political hyperbole to offer a brief explanation of how insurance works. This applies to property, casualty, liability, life, and — yes — health insurance.

Purchasing an insurance policy is an agreement to “share risks” with all the other individuals covered by that insurance company. You pay a premium in order to put money into the “pool.” The premium amount depends on (1) the coverage selected and (2) the x-amount of calculations a company makes to determine how much of a “risk” you are in the pool. For example, if your home’s electrical system hasn’t been updated since the 1970s, there’s a greater chance that the house will explode in flames than a house that updated its electrical system in the past ten years. A homeowner with 1970s electrical wiring will have a higher premium than someone with a recently-updated house.

Money is taken from the pool to cover claims, e.g., a car crash, a basement flood, a gallbladder surgery, and so on. By paying for insurance, you are sharing the cost of covering those claims for others as well as yourself. When you keep up your side of the contract — by paying your insurance premium — you are (pretty much) guaranteed to be covered for all the items outlined in your plan. You pay your premium, you get your coverage.

Not too complicated.

In the case of health insurance, most plans require a copay for a doctor’s visit, prescription refill, and what not. This amount is fixed, is dictated right into the policy, and is what the client pays for the product or service used before the insurance company covers the rest. You pay your premium, you get your coverage, and you are likely responsible for a copay.

So here’s a quick summary of the relevant portions of the ACA. Under the individual mandate, everyone is required to purchase a health insurance plan. When you go to the exchanges (provided the website is functioning), you are going there to browse various insurance plans that you have to pay for (with or without subsidies). According to the health insurance regulations in the ACA, all plans require no copays for birth control. You’re still paying for health insurance — you’re just not forking over money for a copay.

It is disingenuous to claim that removing copays is equivalent to eliminating all out-of-pocket costs.

Where are you getting the money to pay for mandated insurance? It comes from your wallet that’s in your pocket. Due to the new regulations, paying your premium means that you are guaranteed the coverage in your policy — which now includes the proviso that birth control does not require a copay. Getting rid of a copay does not change the fact that you are paying for a policy and merely obtaining the coverage in that policy.

How is paying a premium for an insurance policy that includes zero copay for birth control “free” at all?

Ironically, various outlets cheering the “free birth control” in the ACA gesture towards this paradox.

For example, this article from Jezebel answers the question “when/how do I get my free birth control” by explaining how you enroll in health plans and then don’t “have to pay anything out of pocket for these services. Yay!” Even NARAL states that “free” birth control means making it “available to women at no out-of-pocket cost.”

Nothing out-of-pocket except for the premiums that you’re paying to get that coverage that doesn’t require a copay on these items.

I like my birth control like I like my supermarket samples: #nocost #obamacare http://t.co/dgSWraSy3A

— Lena Dunham (@lenadunham) October 2, 2013

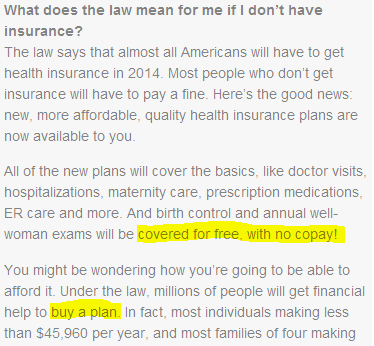

Interestingly, Dunham’s tweet links to Planned Parenthood’s web portal on the Affordable Care Act. If you click on “about the law” and open the “what the law means for you” tab (forgive me, the entire site is flash-based), you can scroll down to this little piece of information that undermines Dunham’s #nocost tag:

Emphasis on “buy a plan.” Birth control is only “covered for free” to the extent that it is now required in all insurance plans and that you don’t have a copay. Yet it does not matter when you are paying in the chain of health insurance transactions. You’re still paying for it.

Getting what you’re paying for in your insurance plan is not “free.”

Provided that one knows how insurance works.